Best Tax-Saving Investments Under Section 123 (Earlier Section 80C): Complete 2026 Guide

Paying taxes is an unavoidable reality for every earning citizen. However, paying more tax than necessary is not something you have to accept.

Every smart taxpayer looks for ways to legally protect their hard-earned money from excessive TDS (Tax Deducted at Source).

The introduction of the Income Tax Act, 2025 has brought some changes, and one of the biggest updates is the transition from the old Section 80C to the new Section 123.

If you want to maximize your take-home salary and build a secure financial future, understanding this new section is absolutely necessary. 💰

What is Section 123?

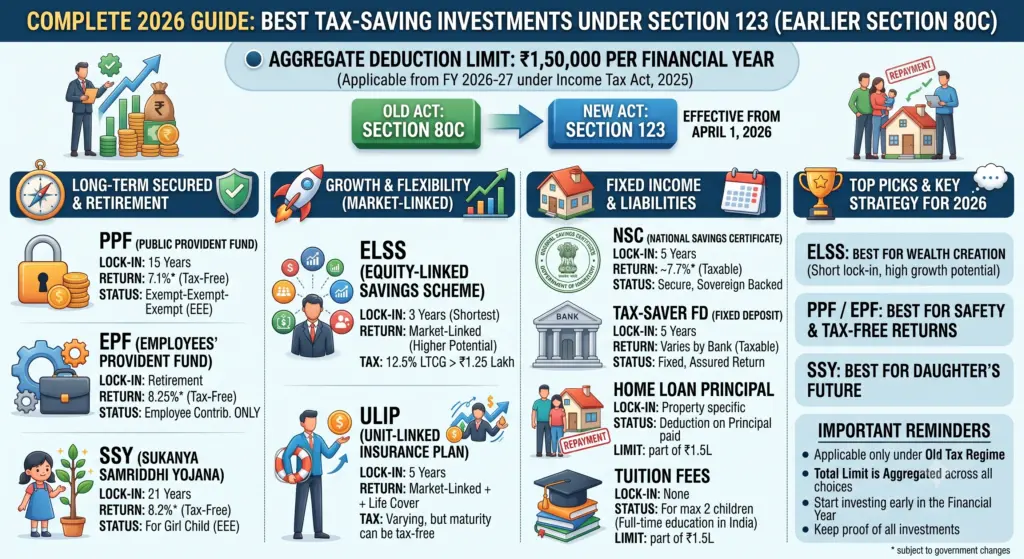

Section 123 of the Income Tax Act, 2025 replaces the former Section 80C.

It allows individual taxpayers and Hindu Undivided Families (HUFs) to claim tax deductions up to ₹1.5 lakh in a tax year.

This deduction applies to specific investments and expenses listed under Schedule XV, such as PPF, EPF, ELSS, life insurance premiums, and home loan principal repayment.

To claim this tax benefit, you must file your returns under the old tax regime.

By utilizing Section 123, you can effectively lower your taxable income while simultaneously creating long-term wealth.

The best part about these investments is that they serve dual purposes.

Not only do they reduce your tax burden, but they also help you fund life goals like retirement, your child’s education, or buying a home.

In this comprehensive guide, we will cover:

- What Section 123 entails in 2026.

- Why Section 80C was renamed.

- Eligibility criteria for claiming deductions.

- The complete list of top 15 tax-saving investments.

- How to match investments with your age and goals.

- Common mistakes to avoid.

Let’s begin exploring the most effective ways to save your tax.

What Is Section 123 (Earlier Section 80C)?

Section 123 is currently the most significant tax-saving provision under the new Income Tax Act, 2025.

It permits eligible taxpayers to reduce their taxable income by investing in specified financial instruments.

The core objective remains identical to the past. The government wants to encourage citizens to save money, invest for the future, and secure their retirement.

How does this actually work for you?

Section 123 allows you to deduct up to ₹1.5 lakh from your total gross income.

Therefore, if your income is ₹10 lakh, investing the full limit brings your taxable income down to ₹8.5 lakh.

This directly reduces your final tax liability.

What are the common options under Section 123?

You have several reliable choices for your money.

These include the Public Provident Fund (PPF), Employees’ Provident Fund (EPF), Equity Linked Savings Scheme (ELSS), and National Savings Certificate (NSC).

In addition, expenses like children’s tuition fees and home loan principal repayments are fully covered.

Why Was Section 80C Renamed to Section 123?

Many taxpayers felt confused when they heard Section 80C was missing from the new budget.

The explanation is actually very simple and straightforward.

The government introduced the Income Tax Act, 2025 to streamline and modernize the six-decade-old tax laws.

Furthermore, they reorganized the chapters and renumbered 819 old sections into just 536 new ones.

Is the tax benefit different now?

No, the financial impact on your wallet remains exactly the same.

The rules, the ₹1.5 lakh deduction limit, and the eligible investment options listed under Schedule XV have barely changed.

| Feature | Earlier Provision | New Provision (2026) |

| Section Name | Section 80C | Section 123 |

| Governing Law | Income Tax Act, 1961 | Income Tax Act, 2025 |

| Maximum Deduction | ₹1.5 lakh | ₹1.5 lakh |

| Primary Goal | Encourage savings | Encourage savings |

Read It

The Complete Guide to the New EPF Scheme 2026: What’s Changing for Employees?

Highlights of Section 123

Understanding the basic rules of Section 123 is the first step in effective tax planning.

The financial year is now officially referred to as the “Tax Year” under the 2025 Act.

Here are the essential facts you must remember:

- Applicable From: Tax Year 2026-27 onwards.

- Maximum Limit: ₹1,50,000 across all combined investments.

- Eligible Regime: Strictly available under the Old Tax Regime.

- Governing Schedule: Investments must align with Schedule XV of the Act.

Who Can Claim Deduction Under Section 123?

Eligibility rules determine exactly who can take advantage of these tax breaks.

The government has clearly defined which taxpayer categories qualify for Section 123 deductions.

Salaried employees represent the largest group of beneficiaries here.

They can use their automatic EPF contributions, life insurance premiums, and tuition fees to lower their taxable salary.

Self-employed individuals are equally eligible to claim these benefits.

Doctors, freelance writers, lawyers, and business owners can invest in PPF or ELSS to save on taxes.

Hindu Undivided Families (HUFs) also enjoy access to these tax-saving provisions.

The Karta of the HUF can invest in eligible schemes in the name of the family members.

Overall, any resident individual meeting the criteria can leverage Section 123.

It is important to note that corporate entities and partnership firms cannot claim deductions under this specific section.

Can You Claim Section 123 Under the New Tax Regime?

This question confuses many people when filing their returns.

The definitive answer is no, you cannot use Section 123 under the new tax regime.

The new tax regime is designed to offer lower tax rates but without the benefit of traditional deductions.

Consequently, if you select the new regime, your ₹1.5 lakh investment will not reduce your taxable income.

Therefore, you must carefully compare both regimes before finalizing your strategy.

Sometimes, the new regime offers a lower final tax bill even without claiming any investments.

On the other hand, if you have a home loan and high insurance premiums, the old regime usually remains the better choice.

Why Is Section 123 Important?

Viewing Section 123 solely as a tax-saving tool is a major mistake.

This section essentially acts as a forced savings plan that builds your wealth over time.

Firstly, it significantly reduces your current tax burden.

For instance, if you fall in the 30% tax bracket, maximizing the ₹1.5 lakh limit saves you roughly ₹46,800 in taxes every single year.

Secondly, it secures your long-term financial independence.

Your PPF balance grows steadily with guaranteed compound interest.

Similarly, ELSS investments harness the power of the stock market to beat inflation.

Sukanya Samriddhi Yojana guarantees a safe fund for your daughter’s future education.

In conclusion, you are paying yourself instead of paying the government.

How Much Tax Can You Save?

Calculating your exact savings requires knowing your current income tax slab.

The higher your income, the more money you save by claiming this deduction.

Here is a quick breakdown of potential savings under the old regime:

| Annual Income | Section 123 Investment | Taxable Income |

| ₹10,00,000 | ₹1,50,000 | ₹8,50,000 |

| ₹12,00,000 | ₹1,50,000 | ₹10,50,000 |

| ₹16,00,000 | ₹1,50,000 | ₹14,50,000 |

Does investing more than ₹1.5 lakh give more tax benefits?

No, the deduction is strictly capped at ₹1,50,000.

Any amount invested beyond this limit in Schedule XV options will not yield additional tax relief under Section 123.

Things to Remember Before Investing

Rushing to buy tax-saving products in March is a terrible financial habit.

Last-minute decisions often result in buying low-return products that lock up your money for years.

Instead, you should follow these proven strategies for success:

- Begin your investments in April at the start of the Tax Year.

- Set up monthly SIPs to avoid a sudden cash crunch later.

- Never buy an insurance policy purely to save tax.

- Read the lock-in period rules carefully before committing your funds.

- Keep all payment receipts safe for ITR verification.

Top 15 Best Tax-Saving Investments Under Section 123

Having multiple choices means you can select the product that perfectly fits your lifestyle.

Schedule XV of the Income Tax Act, 2025 lists over a dozen eligible options.

Let us break down the top 15 choices available in 2026.

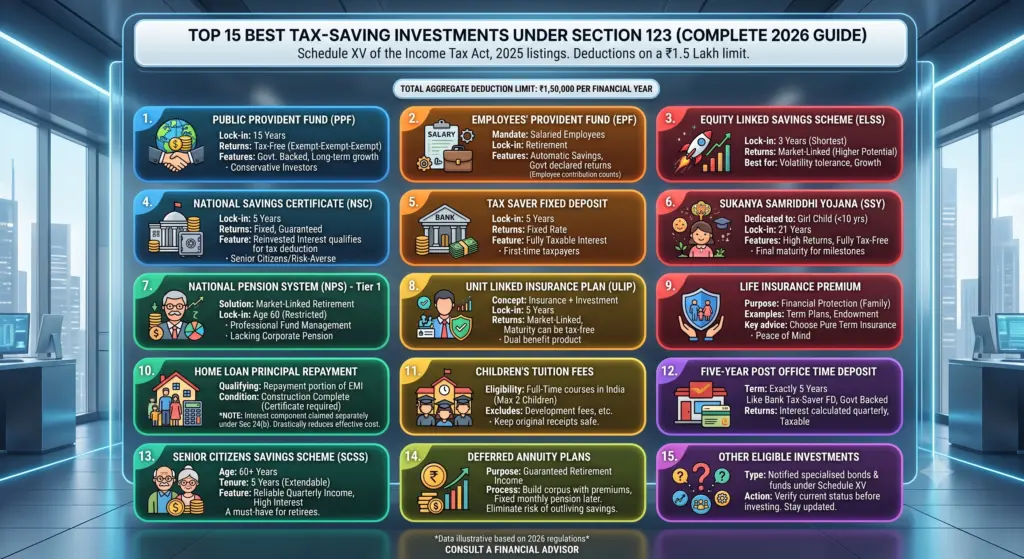

1. Public Provident Fund (PPF)

The Public Provident Fund remains the undisputed king of safe, long-term investments.

Backed by the central government, it provides absolute capital protection alongside tax-free returns.

PPF accounts come with a strict 15-year lock-in period.

However, you can make partial withdrawals after a specified number of years if emergencies arise.

The interest earned on PPF is completely exempt from income tax.

This makes it incredibly powerful for compounding wealth safely. It is best suited for conservative investors who are planning for their retirement.

2. Employees’ Provident Fund (EPF)

The EPF is a mandatory retirement savings scheme for most private-sector employees.

Every month, 12% of your basic salary is automatically deducted and deposited into this account.

Only the employee’s contribution counts toward the Section 123 limit.

The employer’s matching contribution is tracked separately and does not consume your ₹1.5 lakh quota.

This is essentially a hands-free wealth creation tool.

Since the government declares attractive interest rates annually, it forms the bedrock of most salaried individuals’ retirement planning.

3. Equity Linked Savings Scheme (ELSS)

ELSS mutual funds offer the fastest route to high returns among all tax-saving options.

📈 By investing predominantly in the stock market, these funds have historically outperformed inflation and traditional fixed deposits.

The biggest advantage of ELSS is its incredibly short lock-in period.

You only have to leave your money invested for 3 years, which is the lowest across all Section 123 instruments.

However, market-linked investments always carry inherent risks.

Therefore, you should only choose ELSS if you can tolerate short-term volatility and are investing for a horizon of 5 to 7 years.

4. National Savings Certificate (NSC)

The National Savings Certificate is a highly reliable product available at your local post office.

It provides a fixed, guaranteed return that compounds annually over the tenure.

Your money remains locked in for exactly 5 years.

There is no maximum limit on how much you can invest, but the tax deduction is still capped at ₹1.5 lakh.

One unique feature is that the interest earned is reinvested and qualifies for a tax deduction in the subsequent years.

It perfectly suits senior citizens and highly risk-averse individuals.

5. Tax Saver Fixed Deposit

Bank tax-saver FDs are the easiest products to understand and purchase.

Almost every scheduled commercial bank offers these 5-year deposits to their customers.

The return rate is fixed at the time of opening the account.

Consequently, you know exactly how much money you will receive upon maturity.

Unfortunately, the interest you earn on these FDs is fully taxable based on your income slab.

They are best for first-time taxpayers who want complete safety without complex paperwork.

6. Sukanya Samriddhi Yojana (SSY)

The Sukanya Samriddhi Yojana is a brilliant government scheme dedicated to the financial security of the girl child.

Parents or legal guardians can open this account for a daughter aged below 10 years.

It consistently offers higher interest rates compared to PPF and other small savings schemes.

Furthermore, the final maturity amount and the interest earned are entirely tax-free.

The account matures after 21 years from the date of opening.

It is specifically designed to cover major future milestones like higher education and marriage.

7. National Pension System (NPS) – Tier 1

The National Pension System is a highly cost-effective, market-linked retirement solution.

While there is a separate Section 80CCD(1B) / Section 124 for extra NPS benefits, your base contribution also qualifies under Section 123.

It forces you to remain disciplined because withdrawals are heavily restricted until you turn 60.

You can actively choose how much of your money goes into equities versus government bonds.

NPS is highly recommended for anyone who lacks a traditional corporate pension plan.

It builds a massive retirement corpus through professional fund management.

8. Unit Linked Insurance Plan (ULIP)

ULIPs combine the safety of life insurance with the growth potential of mutual funds.

A portion of your premium secures your life cover, while the rest is invested in the equity or debt markets.

These policies come with a mandatory 5-year lock-in period.

Moreover, the maturity proceeds are usually tax-free under specific conditions outlined in the law.

Before purchasing a ULIP, you must carefully evaluate the mortality charges and fund management fees.

They are best for individuals who want a single product for both protection and investment.

9. Life Insurance Premium

Protecting your family’s financial future is the fundamental purpose of life insurance.

🛡️ The premiums you pay for term plans, endowment plans, or whole-life policies qualify for Section 123 deductions.

You should never buy a life insurance policy solely to save on taxes.

The primary goal is to ensure your dependents can maintain their lifestyle if you pass away unexpectedly.

Pure term insurance is always the smartest choice here.

It provides a massive cover amount for a very low annual premium, offering ultimate peace of mind.

10. Home Loan Principal Repayment

Owning a house requires heavy capital, but the government rewards you for taking that step.

🏠 The portion of your EMI that goes toward repaying the principal amount qualifies for the ₹1.5 lakh deduction.

This benefit drastically reduces the effective cost of your property over time.

However, to claim this, the construction of the property must be fully complete, and you must possess the completion certificate.

Can I claim home loan interest under Section 123?

No, Section 123 only covers the principal repayment. The interest component is claimed separately under Section 24(b) of the Income Tax Act.

11. Children’s Tuition Fees

Educating your children is expensive, but it also lowers your taxable income.

The tuition fees paid to any recognized school, college, or university in India are eligible for deduction.

This benefit is restricted to a maximum of two children per taxpayer.

Furthermore, it strictly applies only to full-time education courses.

Keep in mind that development fees, transport charges, and hostel expenses are excluded.

You must keep the original fee receipts safe to prove your claim during tax filing.

12. Five-Year Post Office Time Deposit

The Post Office Time Deposit operates exactly like a bank tax-saver FD but is backed entirely by the government.

It offers a secure avenue to park your funds for exactly five years.

The interest is calculated quarterly but is paid out annually to your savings account.

Just like bank FDs, the interest you earn here will be taxed according to your slab rate.

It is a fantastic option for rural investors or senior citizens who prefer dealing with post offices over private banks.

13. Senior Citizens Savings Scheme (SCSS)

The SCSS is a specialized scheme designed specifically for individuals aged 60 and above.

It provides a regular, reliable quarterly income to help retirees manage their living expenses.

Deposits made into this scheme qualify for Section 123 deductions up to the overall limit.

The scheme has a 5-year tenure, which can be extended for another 3 years upon maturity.

It offers one of the highest interest rates among all guaranteed-return products in India.

Therefore, it is a must-have in every retiree’s financial portfolio.

14. Deferred Annuity Plans

Annuity plans are insurance contracts that guarantee a steady stream of income during your retirement years.

Premiums paid toward eligible deferred annuity plans are fully deductible under Section 123.

You pay premiums during your earning years to build the corpus.

Later, the insurance company pays you a fixed monthly pension when you retire.

It is particularly useful for people who want to eliminate the risk of outliving their savings.

15. Other Eligible Investments

The government occasionally notifies other specialized bonds and funds under Schedule XV.

For instance, specific infrastructure bonds or notified pension funds may also qualify.

You must always verify the current notification status before investing in these lesser-known instruments.

Staying updated with the latest CBDT circulars ensures your claims are never rejected.

Explore It

Comparison of Popular Section 123 Investments

Comparing your options side-by-side helps clarify which product aligns with your risk appetite.

| Investment | Risk Level | Lock-in Period | Return Type | Best For |

| PPF | Very Low | 15 Years | Fixed, Tax-Free | Safe Retirement |

| EPF | Very Low | Till Retirement | Fixed, Tax-Free | Salaried Employees |

| ELSS | High | 3 Years | Market-Linked | Wealth Creation |

| NSC | Very Low | 5 Years | Fixed, Taxable | Conservative Savers |

| Tax Saver FD | Low | 5 Years | Fixed, Taxable | First-time Investors |

| NPS | Moderate | Till 60 Years | Market-Linked | Pension Planning |

How to Choose the Best Tax-Saving Investment Under Section 123

Picking the correct investment requires analyzing your personal financial landscape.

There is no single universal product that fits the needs of a 25-year-old and a 55-year-old equally.

In Your 20s

Your greatest asset at this age is the long time horizon ahead of you.

Since retirement is decades away, you can easily withstand market volatility to chase higher returns.

Consequently, your primary focus should be on ELSS and NPS.

These equity-heavy instruments will compound massively over the next 30 years.

You should also start a small PPF account simply to initiate the 15-year clock early.

In Your 30s

Life generally becomes more complex and expensive during your thirties.

You might be paying off a home loan, raising young children, or supporting aging parents.

Your strategy must shift toward balancing growth with absolute financial protection.

Claiming your Home Loan principal, paying for Term Life Insurance, and keeping ELSS SIPs active is the ideal mix here.

In Your 40s

Your earning capacity usually peaks during this pivotal decade.

However, your financial obligations, like your children’s higher education, also reach their maximum point.

Stability and predictability become highly crucial at this stage.

You should rely heavily on EPF, PPF, and the deduction you get from your children’s tuition fees to max out the ₹1.5 lakh limit.

In Your 50s and Beyond

Capital preservation is the only rule that matters as you approach retirement.

You cannot afford to lose your accumulated wealth to sudden stock market crashes.

Therefore, you must shift your focus entirely to safe, fixed-income assets.

Products like NSC, Tax Saver FDs, and eventually the Senior Citizens Savings Scheme are perfect for this phase of life.

Tax-Saving Strategies for Salaried Employees

Salaried workers often possess a built-in advantage due to mandatory EPF deductions.

However, relying on EPF alone rarely exhausts the full ₹1.5 lakh limit unless your basic salary is exceptionally high.

A smart salaried professional diversifies their remaining quota across different asset classes.

Here is a highly effective model portfolio:

- EPF Contribution: ₹70,000 (Automatic safety)

- ELSS SIPs: ₹40,000 (Market growth)

- Term Insurance: ₹20,000 (Family protection)

- PPF Deposit: ₹20,000 (Tax-free compounding)

This balanced approach guarantees liquidity, aggressive growth, and total peace of mind.

Tax-Saving Strategies for Self-Employed Individuals

Freelancers and business owners operate without the safety net of corporate EPF.

Thus, they bear the total responsibility of building their own retirement funds from scratch.

Since business income fluctuates, flexibility in investment amounts is vital.

An optimal strategy for a business owner looks like this:

- PPF Deposit: ₹70,000 (Creates a risk-free foundation)

- ELSS Investments: ₹50,000 (Beats inflation)

- NPS Tier 1: ₹30,000 (Locks away money for old age)

By manually creating this structure, self-employed workers can mimic the security of a corporate job.

How to Maximize Your Tax Savings

Saving tax efficiently is a year-long process, not a one-day event.

Many taxpayers lose out on potential wealth simply because they lack a systematic approach.

1. Start Investing Early

April is the best month to plan your taxes. Initiating Monthly SIPs spreads your financial burden evenly across 12 months, preventing a sudden cash shortage in March.

2. Diversify Your Investments

Putting all your money into one single asset is highly risky. Mixing safe government bonds with market-linked equity funds creates a robust portfolio that survives economic downturns.

3. Review Your Portfolio Every Year

Your income and liabilities will inevitably evolve over time. You must adjust your asset allocation annually to reflect changes like a new baby, a salary hike, or a cleared mortgage.

4. Invest According to Your Goals

Tax saving should merely be a byproduct of your actual financial planning. You should buy an asset because it helps you buy a house or retire comfortably, not just because it saves TDS.

5. Keep Proper Records

The Income Tax Department relies heavily on digital matching and verification. You must maintain neat digital folders containing your premium receipts, bank certificates, and school fee challans.

Common Mistakes to Avoid

Avoiding errors is just as important as making the right investments. Millions of rupees are lost every year because taxpayers fall into predictable traps.

Waiting until the last minute forces you into terrible financial decisions. Desperate taxpayers often buy expensive endowment policies from pushy agents just to get a quick receipt before the deadline.

Buying insurance solely for tax benefits is a fundamental flaw in financial logic. If a policy mixes insurance with investment, it usually provides very low life cover and mediocre returns.

Ignoring lock-in periods can destroy your emergency cash flow. If you put your emergency fund into a 15-year PPF account, you will face severe liquidity issues during a crisis.

Forgetting to check the new tax regime is a modern mistake. If you opt for the new regime while filing, your Section 123 investments will not fetch you any tax relief.

Example of Tax Saving Under Section 123

Let us illustrate these rules with a practical, real-world example.

Consider Rahul, a 35-year-old IT professional earning ₹14,00,000 annually. He wants to optimize his taxes under the old regime for Tax Year 2026-27.

He intelligently distributes his money across different sectors.

- He pays ₹45,000 toward his home loan principal.

- His mandatory EPF deduction is ₹55,000.

- He invests ₹30,000 in an ELSS fund.

- He pays ₹20,000 for a term life insurance policy.

His total eligible investment equals exactly ₹1,50,000. Consequently, his taxable income drops from ₹14 lakh down to ₹12.5 lakh, saving him thousands of rupees in the 30% tax bracket.

Final Thoughts

Section 123 of the Income Tax Act, 2025 carries forward the glorious legacy of Section 80C.

It continues to act as the primary wealth-building and tax-saving engine for millions of Indian taxpayers who prefer the old tax regime.

By allowing a generous ₹1.5 lakh deduction, the government actively rewards you for being financially responsible.

The secret to success lies in proactive planning rather than last-minute panic.

If you align your investments with your specific life stage, your money will grow exponentially while your tax liability shrinks.

Ultimately, the true goal of Section 123 is not just saving TDS today, but ensuring you achieve total financial freedom tomorrow.

Frequently Asked Questions

Is Section 80C removed?

No, it has merely been renumbered. Under the new Income Tax Act, 2025, the exact same benefits are now found under Section 123.

What is the maximum deduction under Section 123?

The absolute upper limit is ₹1.5 lakh per tax year. This limit applies to the combined total of all eligible investments made under Schedule XV.

Can I claim Section 123 under the new tax regime?

Generally, you cannot. The new tax regime offers lower standard tax rates but specifically disallows most deductions, including Section 123.

Which investment has the shortest lock-in period?

ELSS mutual funds feature the shortest lock-in duration. Your money is completely accessible after just 36 months.

Can I invest in multiple Section 123 schemes?

Yes, you can diversify freely. However, your total combined claim during ITR filing cannot exceed the ₹1.5 lakh threshold.

Leave a Reply