The Future of Finance: Understanding Tokenization and Wholesale Digital Assets in 2026

The world of money and investments is changing very fast.

You might have heard terms like “tokenization” or “wholesale digital assets” in the news.

While these words sound complicated, they are actually very simple to understand.

Now, in 2026, these technologies are moving from experiments to real-world use.

They are helping banks and big companies move money and assets faster than ever before.

Let’s dive in and look at what this means and why it matters to you.

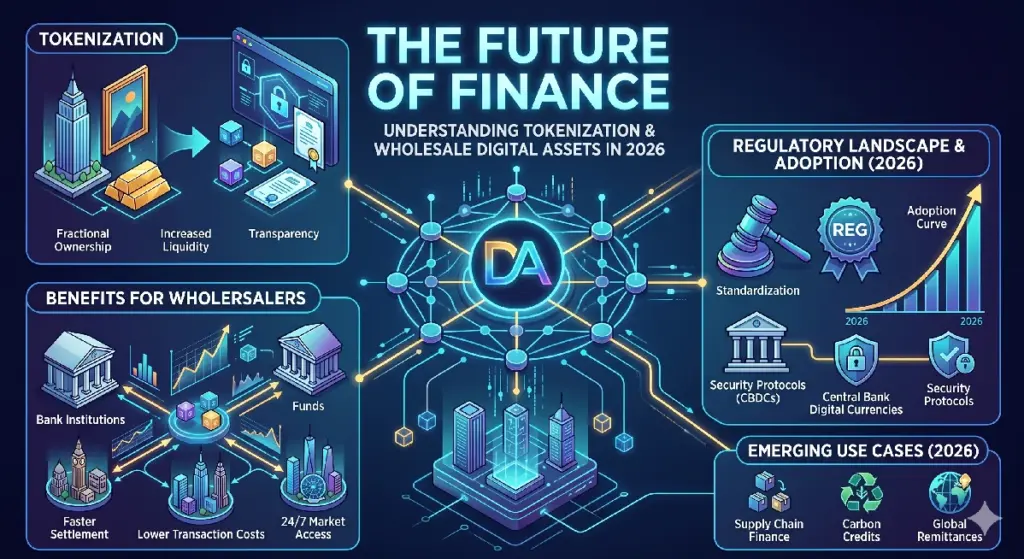

What is Tokenization?

Imagine you own a house or a piece of art. It is hard to sell just a tiny part of it, right?

Tokenization solves this problem.

Simply put, it is the process of taking a real-world asset and turning it into a “token” on a computer network called a blockchain.

Think of this token as a digital certificate of ownership.

Because it is digital, you can easily divide this asset into smaller pieces.

As a result, it becomes much easier for people to buy and sell things that were previously hard to trade.

Pro tip: Tokenization isn’t just for digital coins; it is now being used for real-world assets like bonds, stocks, and even real estate.

Wholesale Digital Assets: Behind the Scenes

While you and I use money for daily shopping, large financial institutions like banks do something different.

They move massive amounts of money and securities between each other every single day.

This is called “wholesale” finance.

Traditionally, this process is slow.

It involves many middlemen, lots of paperwork, and it can take days to settle a single transaction.

Here’s the deal: Wholesale digital assets are the modern answer to this delay.

Instead of sending messages back and forth, banks can now move digital tokens that represent cash or assets.

Because these tokens live on a shared digital ledger, the transfer happens almost instantly.

In other words, it is like the difference between sending a physical letter through the mail and sending an instant email.

Explore this related post

Smart Strategies for Modern Investing in 2026

Why is this happening now?

Most importantly, 2026 is the year of action.

Recent data shows that the market for active tokenized assets has surged significantly, with billions of dollars moving onto the blockchain.

Many central banks and big financial institutions are now building their own versions of this technology.

One major reason is efficiency.

By using “smart contracts“—which are just digital agreements that run automatically—banks can eliminate the need for manual checks.

Furthermore, we are seeing three main types of digital money growing side-by-side this year:

- Wholesale CBDCs: These are digital versions of money issued directly by a central bank. They act as the “gold standard” for settling debts between big banks. IMF eLibrary – International Monetary Fund

- Tokenized Deposits: These are digital versions of the money already sitting in your bank account. They allow banks to offer the speed of crypto with the safety of traditional banking. IMF eLibrary – International Monetary Fund

- Regulated Stablecoins: These are digital tokens backed by safe assets like government bonds. Bottom line, they are becoming very popular for global trade because they are reliable and easy to use across borders. IMF eLibrary – International Monetary Fund

The Real-World Impact

You might be wondering how this affects the average person.

While wholesale assets are for banks, the ripple effects reach everyone.

First, these technologies make the entire financial system more stable.

When banks can settle transactions instantly, there is less risk that something will go wrong in the middle of a trade.

Second, it lowers costs. All those middlemen and slow manual processes in traditional finance cost money. By making these systems faster and more automated, banks can save billions. What this means for you is that these efficiency gains could eventually lead to cheaper services and faster transactions for your personal banking needs.

Third, it opens up new doors. As we move into the second half of 2026, more assets are becoming “liquid.” Thus, it is becoming easier to turn investments into cash. Whether it is real estate, private debt, or even carbon credits, tokenization makes it possible for more people to participate in markets that were once reserved only for the very wealthy.

Looking Ahead: 2026 and Beyond

We are now past the stage of just talking about this technology.

According to recent industry reports, 2026 is the year of “action.”

Financial institutions are busy building the “plumbing” of this new system.

They are working on ways to make sure different networks can talk to each other.

This is called interoperability, and it is the final piece of the puzzle.

Without it, we would just have new, separate islands of technology.

With it, we get a connected, global network that works 24/7.

It’s essential to note that the transition won’t happen overnight, but the path is clear.

Just like the internet changed how we share information, tokenization is changing how we store and move value.

It is a fundamental shift toward a system that is more transparent, faster, and more accessible.

As we look at the progress made so far, it is exciting to see how these digital tools are slowly but surely building a better financial future for everyone.

Let’s explore this further: As we witness this shift toward programmable finance, which aspect of tokenization. The speed of settlement or the ability to fractionalize assets. Do you think will have the biggest impact on the average investor in the coming years?

In short, settlement speed makes the machine run smoother, but fractionalization changes who is allowed to play the game.

Do you think the mainstream adoption of fractionalized real estate, in particular, will change how you structure your own investment strategy?

My Take:

While both are transformative, the ability to fractionalize assets will likely have the most profound impact on the average investor.

- Democratization of Opportunity: Fractionalization lowers the barrier to entry, allowing retail investors to gain exposure to high-value assets—like premium real estate, private equity, or fine art—that were previously reserved for the wealthy. Polymesh network

- Enhanced Portfolio Diversification: By breaking large, expensive assets into smaller, affordable units, investors can build more diversified portfolios with limited capital, effectively spreading their risk across asset classes that were once “out of reach.” Polymesh network

- The “Speed” Context: While faster settlement (near-instantaneous trade finality) is a significant improvement in efficiency and reduces counterparty risk, it is primarily a benefit of “market plumbing.” For most retail investors, the ability to access new and diverse investment vehicles via fractional ownership is a far more tangible, life-changing shift than reducing settlement time from days to minutes.

In short, settlement speed makes the machine run smoother, but fractionalization changes who is allowed to play the game.

Do you think the mainstream adoption of fractionalized real estate, in particular, will change how you structure your own investment strategy?

Leave a Reply