Understanding Fintech and Digital Assets: A Simple Guide for Everyone

Welcome to the Future of Money

I wanted to write about this because the world is moving fast, and the way we handle money has changed forever.

Nowadays, we rarely carry fat wallets full of cash.

Instead, we carry smartphones.

In today’s world, missing out on how money is shifting means getting left behind.

The global economy is facing a massive transformation, making it the perfect time to understand these changes.

Furthermore, this shift is massive.

Indeed, the global fintech market is exploding, valued at $460.76 billion this year in 2026.

Top 5 Fintech Companies Globally

To illustrate how large this space has become, here are the top 5 powerhouse companies leading the fintech world today:

- Stripe: A giant infrastructure platform that handles online payments for millions of businesses.

- Visa / Mastercard: Traditional network giants that have successfully transformed into digital payment leaders.

- Revolut: A massive global banking “super-app” that recently secured a landmark $3 billion valuation boost.

- PayPal / Block (Square): Everyday consumer names that changed how small businesses and individuals send money.

- Nubank: The largest digital bank in Latin America, completely changing how an entire continent handles finances.

Why You Need This Knowledge Today

Let’s start with a simple truth: financial literacy is no longer just about balancing a checkbook.

Importantly, knowing about fintech and digital assets is necessary because traditional banking is fading away.

Because of this shift, jobs, businesses, and everyday shopping require digital knowledge.

Moreover, if you do not understand digital assets, you might miss out on modern ways to grow your wealth.

Significantly, artificial intelligence (AI) and blockchain are now running the platforms we use daily.

Therefore, learning this now keeps your money safe and your skills relevant.

Read It

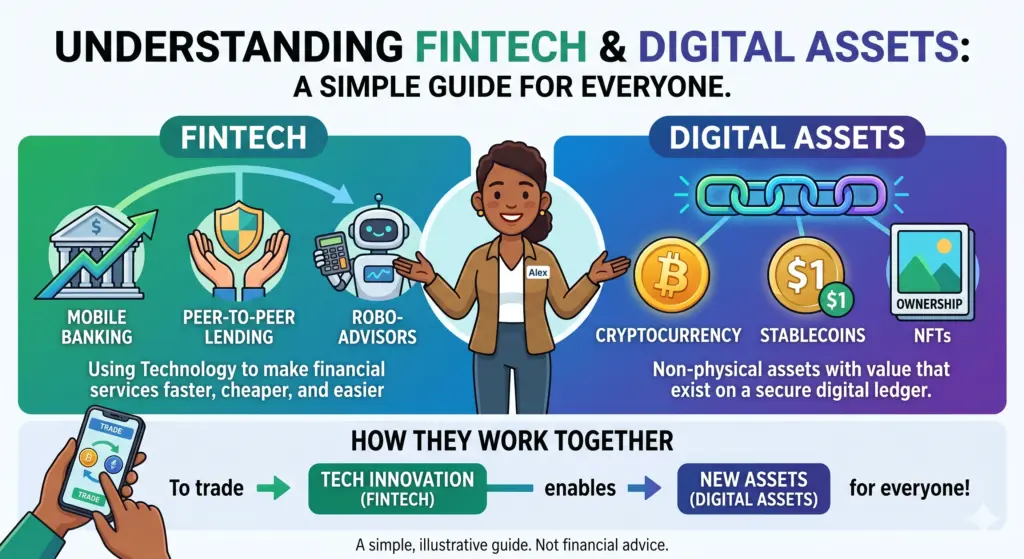

What is Fintech?

Initially, the word “Fintech” might sound complex, but it is just a blend of "Financial" and "Technology."

In short, it is any software, mobile app, or online tool that helps you manage your money without visiting a physical building.

For Examples

- Mobile Payments: Sending money instantly to a friend using an app on your phone. For instance, India’s UPI ecosystem is so massive that it processed over

106 billion transactionsin just the first half of last year.

- Digital Lending: Getting a small business loan approved by an app in five minutes instead of waiting weeks at a bank.

- Online Investing: Using platforms like Robinhood or Groww to buy fractional shares of stock with a few taps.

The Latest Data

Fintech is no longer an experiment; it is the new standard.

[Global Fintech Market Value in 2026] ---> $460.76 Billion

[AI-Driven Fintech Funding] ---> $16.8 Billion (Invested in smart fraud detection & AI tools)

Consequently, banks are forcing themselves to adapt.

In fact, traditional banks now hold a 36.9% share of the fintech market.

Because they are partnering with tech startups to survive.

Explore It

What are Digital Assets?

On the other hand, if fintech is the digital tool or highway, digital assets are the new kinds of money or property traveling on that highway.

Simply speaking, a digital asset is anything of value that exists strictly in a digital format and comes with a clear right to use or ownership.

For Examples

- Cryptocurrencies: Digital currencies like Bitcoin that operate on decentralized networks.

- Stablecoins: Digital tokens tied directly to stable real-world assets, such as the US Dollar. They give you the speed of crypto without the wild price swings.

- Tokenized Real-World Assets (RWA): This is a massive trend in 2026. To illustrate, companies are taking a physical item, like a luxury apartment building, and breaking it down into digital tokens. Then, everyday people can buy a tiny fraction of that property online.

Some facts on Digital Assets

The infrastructure to manage these assets is growing rapidly.

Specifically, the global digital asset management market size has climbed to $6.29 billion in 2026.

Global data creation is hitting unprecedented heights.

Businesses now rely on secure, cloud-based digital ledgers.

These tools track who owns what.

How Fintech and Digital Assets Work Together

Although, you can look at these two concepts as two sides of the same coin.

They are deeply correlated and rely on each other to succeed.

The Highway & The Car Analog: Think of Fintech as the high-tech digital highway system (the apps, payment rails, and security software). Think of Digital Assets as the modern vehicles driving on that highway.

First, fintech apps provide the user-friendly screens and interfaces that allow everyday people to buy, sell, and store digital assets easily.

Second, digital assets provide the backend technology (like blockchain) that allows fintech companies to move money across international borders in seconds instead of days.

As a result, they are fusing together to create a faster, fairer financial world.

Your Simple, Step-by-Step Guide to the New Era

To wrap it all up, here is a quick summary guide of how this changing world impacts you:

- Step 1: Get Connected: All you need is a basic smartphone and an internet connection to access the global economy.

- Step 2: Embrace Financial Inclusion: Fintech is bringing millions of unbanked people into the system. You can now save, borrow, and get paid securely without needing a local physical bank branch.

- Step 3: Watch the Tech Fusion: In 2026, the line between an app and a bank has completely vanished. Traditional financial systems are fully digital now.

- Step 4: Stay Secure: Above all, always remember that because money is digital, cybersecurity and fraud monitoring are highly critical. Look for apps that use AI to protect your accounts in real-time.

In conclusion, technology is finally making money work for everyone, everywhere.

Overall, staying curious and understanding these tools will give you the power to grow your savings and protect your financial future.

Leave a Reply