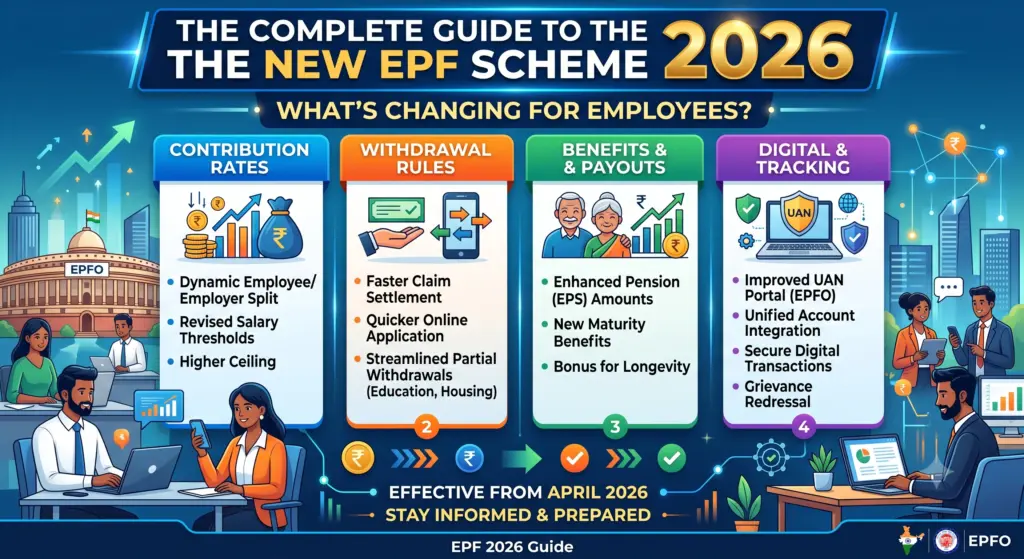

The Complete Guide to the New EPF Scheme 2026: What’s Changing for Employees?

Have you recently heard about the New EPF Scheme 2026 and wondered whether your PF account will change?

Millions of salaried employees across India are asking the exact same questions today.

The government introduced the Employees’ Provident Funds Scheme, 2026, under the broader Code on Social Security, 2020.

This major legal update officially replaces the old Employees’ Provident Funds Scheme of 1952. While the change sounds massive, most employees do not need to panic.

Your hard-earned money remains completely safe.

However, the new framework brings significant updates to how you manage, withdraw, and track your retirement funds.

In this comprehensive guide, we will break down every single detail you need to know.

The New EPF Scheme 2026 modernizes provident fund rules under the Code on Social Security.

While the mandatory 12% contribution remains unchanged and capped at the statutory wage ceiling, contributions above this limit are entirely voluntary.

A major update to PF Withdrawal Rules allows members to withdraw up to 75% of their balance for medical, education, or housing needs, provided they maintain a 25% minimum balance.

Furthermore,

100% full withdrawal requires 12 months of continuous unemployment.Overall, the new framework prioritizes digital compliance, faster claim processing, and seamless account portability.

What is the new EPF scheme for 2026?

The government has officially notified the New EPF Scheme 2026 to modernize India’s social security framework.

For more than 70 years, the EPF Scheme of 1952 governed how private-sector workers saved for retirement.

Since then, the workplace has changed drastically.

Today, employees switch jobs frequently, rely on digital banking, and demand faster access to their funds.

To begin with, the new 2026 scheme aligns provident fund rules with the modern digital era.

It legally integrates the EPF into the new labour codes passed by the parliament.

The primary goal is to ensure faster claim settlements, tighter digital security, and better transparency for all subscribers.

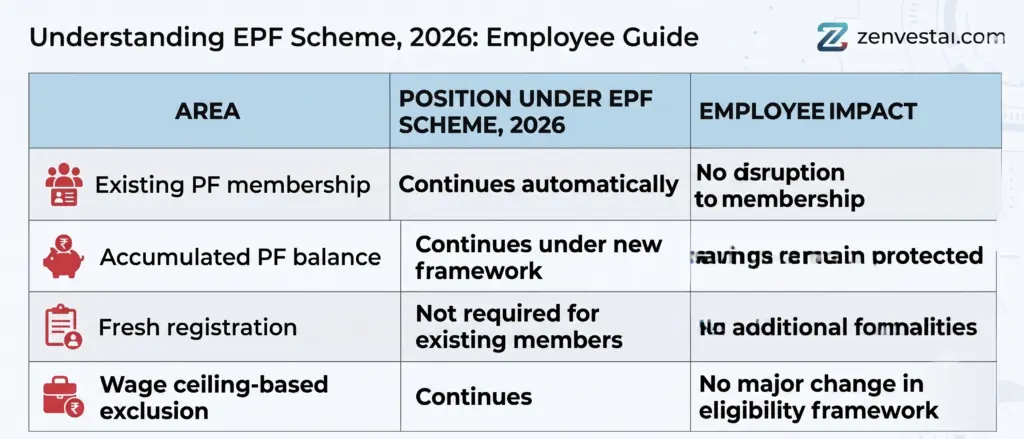

The core structure of your provident fund remains entirely the same.

You still have a Universal Account Number (UAN) that tracks your savings.

You still earn an annual interest rate declared by the government.

Your employer still matches your basic contribution.

However, the administrative machinery running behind the scenes has been completely overhauled.

Consequently, you will experience less paperwork, fewer manual approvals, and significantly faster processing times when you interact with the Employees’ Provident Fund Organisation (EPFO).

Why did the government feel the need to replace a 70-year-old system?

In the past, managing EPF involved physical forms, long waiting periods, and fragmented records.

When people changed jobs, they often ended up with multiple inactive PF accounts.

Furthermore, tracking employer defaults was difficult for the average worker. The new scheme fixes these historical loopholes.

It mandates strict digital compliance for employers.

It heavily relies on Aadhaar-based verification.

Ultimately, the new framework shifts the power back to the employees, allowing them to control their retirement funds directly from their smartphones.

Learn more about

Government Securities in India: A Beginner’s Guide to Safe Investing

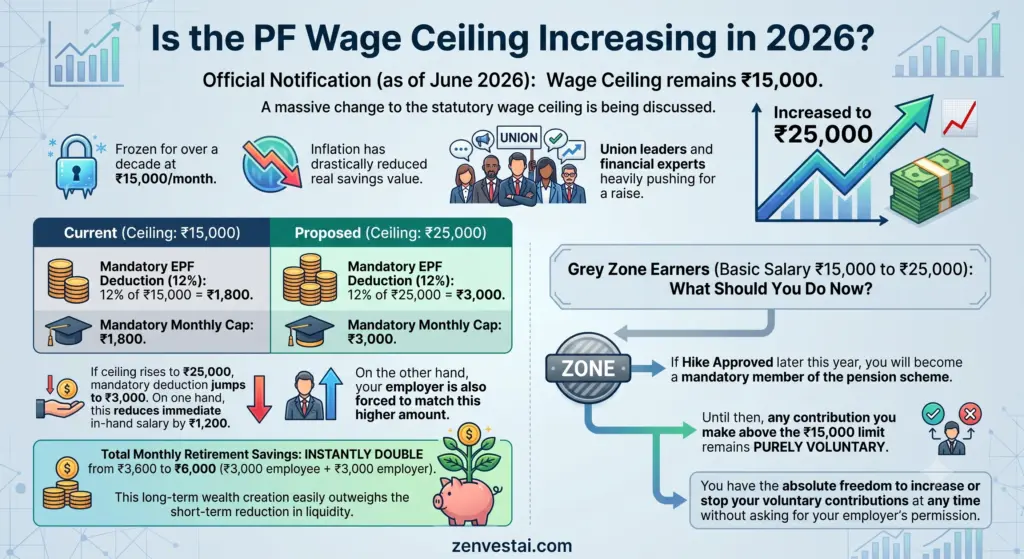

Is the PF wage ceiling increasing in 2026?

A massive change regarding the EPF wage ceiling is currently being discussed in policy circles.

For over a decade, the statutory wage ceiling has remained frozen at ₹15,000 per month.

This means that mandatory EPF deductions are only legally required on the first ₹15,000 of your basic salary.

Meanwhile, inflation has drastically reduced the real value of these savings.

Union leaders and financial experts have heavily pushed the government to raise this limit.

If the limit increases to ₹25,000, more money will automatically go into your provident fund every month 📈.

How does the statutory wage ceiling actually impact your monthly take-home pay?

Let us look at a practical example.

Currently, 12% of ₹15,000 equals ₹1,800.

Therefore, the mandatory monthly deduction for many employees is capped at ₹1,800.

If the ceiling rises to ₹25,000, the mandatory deduction jumps to ₹3,000.

On one hand, this reduces your immediate in-hand salary by ₹1,200.

On the other hand, your employer is also forced to match this higher amount.

As a result, your total monthly retirement savings would instantly double.

This long-term wealth creation easily outweighs the short-term reduction in liquidity.

As of the official June 2026 notification, the wage ceiling remains at ₹15,000.

However, the government has kept the legal provisions ready within the new scheme to update this ceiling seamlessly in the future.

Employees who earn salaries falling in the “grey zone” between ₹15,000 and ₹25,000 need to pay close attention.

If the hike is approved later this year, you will become a mandatory member of the pension scheme.

Until then, any contribution you make above the ₹15,000 limit remains purely voluntary.

You have the absolute freedom to increase or stop your voluntary contributions at any time without asking for your employer’s permission.

How Do EPF Contributions Work Under the New Scheme?

Understanding your monthly EPF contribution is the first step toward effective financial planning.

Every single month, a specific portion of your salary is deducted and sent to the EPFO.

In addition, your employer is legally required to deposit a matching amount.

For most established companies, the standard contribution rate is set at 12% of your Basic Salary plus Dearness Allowance (DA).

Some smaller companies or specific industries might operate on a 10% rate, but the 12% rule applies to the vast majority of the corporate workforce.

Your employer’s 12% matching contribution does not go straight into your PF balance.

This is a very common misconception that confuses millions of young professionals.

The employer’s share is actually split into two different buckets.

Specifically, 3.67% goes directly into your main EPF account to build your lump-sum retirement corpus.

The remaining 8.33% goes into the Employee Pension Scheme (EPS).

This EPS portion builds a separate fund that will pay you a guaranteed monthly pension after you retire.

Therefore, your total retirement safety net is actually composed of two distinct financial products working together.

Let us illustrate this with a simple mathematical breakdown.

Assume your basic salary is exactly ₹15,000 per month.

You will contribute 12% of this amount, which equals ₹1,800. This entire ₹1,800 goes into your EPF account.

Next, your employer matches the ₹1,800.

However, ₹1,250 (which is 8.33% of ₹15,000) goes into your EPS pension account.

The remaining ₹550 (which is 3.67% of ₹15,000) goes into your EPF account.

Over time, your EPF account earns compound interest, while your EPS account secures your future monthly payout.

Read our full guide on

The Concept of Voluntary Provident Fund (VPF)

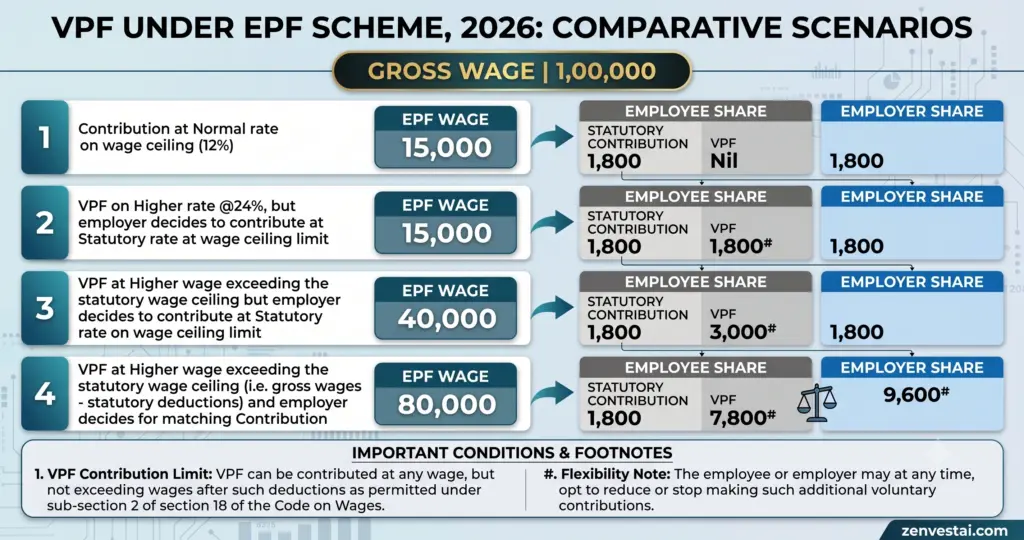

What if you want to save more money for your retirement?

The new scheme makes the Voluntary Provident Fund (VPF) much easier to manage.

If you wish to contribute more than the mandatory 12%, you can easily instruct your HR department to deduct a higher percentage.

You can even choose to contribute up to 100% of your basic salary.

The best part is that this extra money earns the exact same high interest rate as your regular EPF.

Moreover, the VPF enjoys excellent tax benefits.

Thus, it serves as one of the safest and most profitable fixed-income investments available in India today.

What Are the New PF Withdrawal Rules?

Accessing your money when you truly need it is a critical feature of the New EPF Scheme 2026.

The government recognizes that life is unpredictable.

Sometimes, you face sudden medical bills, housing needs, or periods of unemployment.

Previously, the withdrawal rules were incredibly complex, featuring 13 different sub-categories and confusing paperwork.

Now, the new scheme simplifies everything into clear, digital-first processes.

The most important new rule is the mandatory 25% minimum balance requirement for partial withdrawals.

What does the 25% minimum balance rule actually mean for you?

Under the new scheme, you cannot drain your account completely during a partial withdrawal.

The EPFO calculates your “eligible member balance” by first locking away 25% of your total funds.

For example, if you have ₹1,00,000 in your account, ₹25,000 must remain untouched.

You are only allowed to withdraw funds from the remaining ₹75,000.

This rule ensures that you always have a baseline retirement corpus growing in the background, even after you face a financial emergency.

Can I withdraw my full PF amount in 2026?

You cannot empty your entire provident fund account immediately just because you left your job.

The government strictly treats the EPF as a retirement fund, not a regular savings account.

Therefore, to withdraw 100% of your accumulated EPF balance, you must prove that you have been continuously unemployed for 12 months 🏦.

This long waiting period discourages people from prematurely spending their retirement money between casual job switches.

What happens if you need urgent cash immediately after losing your job?

The system does offer a fair compromise.

If you lose your employment, you are permitted to withdraw up to 75% of your available funds almost immediately.

This provides a crucial financial cushion to help you survive while you search for a new job.

The remaining 25% stays safely locked in the account.

If you remain unemployed for the full 12 months, you can then apply to withdraw that final 25%.

However, if you find a new job within those 12 months, you simply transfer the remaining balance to your new employer.

Medical Emergencies

Medical emergencies require immediate financial support without bureaucratic delays.

Under the 2026 framework, you can apply for a medical advance to cover major surgeries, hospitalizations, or serious illnesses.

This benefit extends to your own treatment as well as the treatment of your immediate family members.

Because medical claims are time-sensitive, the EPFO prioritizes them in the digital queue.

You do not need to submit heavy medical files online; a simple doctor’s certificate and a self-declaration are usually sufficient to trigger the release of funds.

Housing and Construction

Buying a house is a major milestone that requires significant capital.

The EPF scheme allows eligible members to use their savings to purchase a plot of land, buy a flat, construct a new house, or even repay an existing home loan.

To qualify for a housing withdrawal, you generally need to complete a minimum number of years in service (usually 5 years).

The funds are paid directly to the housing agency or the bank in most cases.

Additionally, you can withdraw funds for major home renovations or structural repairs, provided you meet the specific conditions outlined in the EPFO guidelines.

Higher Education and Marriage

Higher education expenses can drain your regular savings very quickly.

If you or your children are pursuing higher studies, you can tap into your EPF balance.

The education landscape is expensive.

Even if a student secures a tuition waiver, grant, or monthly stipend, the upfront costs can be heavy.

You might need funds to pay for admission fees, travel, or preparing a comprehensive SOP (Statement of Purpose) for foreign universities.

The EPFO allows you to withdraw a portion of your funds to cover these genuine educational costs.

Similarly, you can withdraw money to cover the marriage expenses of yourself, your children, or your siblings.

What Has Changed in the New EPF Scheme 2026?

Digital records have become the absolute backbone of the new EPF ecosystem.

The government has launched a massive initiative to move every single EPFO service online.

In the past, you had to visit the PF office, stand in long queues, and submit physical forms attested by your employer.

Today, the new scheme mandates a digital-first approach.

Claims, transfers, KYC updates, and employer filings are all handled through the unified member portal.

This massive shift cuts down processing times from several weeks to just a few days.

Faster claim processing is arguably the biggest relief for salaried workers.

Previously, a final PF settlement could take up to a month.

Now, the system uses automated algorithms to process routine partial withdrawals.

If your KYC is perfectly updated, the system can clear your medical or education advance in less than a week.

The new framework enforces strict turnaround times for EPFO officials.

Consequently, your money reaches your bank account much faster during critical moments of need.

Your Aadhaar number is now the most critical piece of your PF identity.

The 2026 scheme places massive importance on Aadhaar-linked verification.

By linking your UAN with your Aadhaar, the EPFO instantly verifies your biometric identity.

This completely eliminates the problem of duplicate accounts and deeply reduces the risk of financial fraud.

You must ensure that the name, date of birth, and gender on your Aadhaar card perfectly match the details registered in your EPF account.

Even a minor spelling mistake can cause the automated system to reject your claim.

Employers now face much stricter compliance rules and severe penalties for delays.

The government wants to protect employees from companies that deduct PF money from salaries but fail to deposit it into the EPFO.

Under the new Code on Social Security, employers must maintain impeccable digital records and file their returns on time.

If a company delays the monthly deposit, the system automatically flags the default and calculates penal damages.

This increased transparency ensures that your hard-earned money is safely deposited every single month without fail.

How Does Job Switching Affect Your EPF?

What happens when you decide to switch jobs in the modern corporate world?

In the past, changing employers often meant opening a brand new PF account and leaving the old one behind.

Millions of rupees are currently lying unclaimed in the EPFO because people forgot their old account details.

The new scheme solves this permanently by emphasizing the Universal Account Number (UAN).

Your UAN is a unique, 12-digit permanent number that stays with you for your entire working life, regardless of how many times you change companies.

When you join a new company, you simply provide your existing UAN to your new HR department.

They will link your new member ID to this central UAN. All your previous service history and your accumulated balance remain intact.

More importantly, the transfer of funds from the old employer’s account to the new employer’s account is now entirely digital.

You can initiate a transfer request directly from the member portal.

Never withdraw your PF money when you switch jobs; always transfer it to ensure your pension service history remains unbroken.

Can you actually have multiple PF accounts at the same time?

Yes, it is quite common.

If you worked for three different companies in the past, you likely have three different member IDs.

However, as long as all these member IDs are linked under your single UAN, your money is safe.

The member portal allows you to view the passbook for each individual member ID.

To maximize your compound interest and keep things organized, you should consolidate all your old accounts by transferring their balances into your active, current account.

Employee Pension Scheme (EPS) Explained

What is the Employee Pension Scheme (EPS) and why does it matter so much?

Many employees obsess over their EPF balance but completely ignore their EPS account.

As mentioned earlier, 8.33% of your employer’s contribution funds your EPS.

This scheme guarantees a monthly pension after you reach the age of 58.

To be eligible for this lifelong pension, you must complete a minimum of 10 years of eligible service.

This 10-year rule is exactly why transferring your PF account during a job change is so critical.

If you constantly withdraw your money, your service history resets to zero.

Calculating your exact pension amount can seem slightly complicated.

The formula depends on your pensionable salary and your total years of pensionable service.

Currently, the maximum pensionable salary is capped at ₹15,000.

If the government eventually raises the wage ceiling to ₹25,000, your potential monthly pension will increase dramatically.

In the unfortunate event of the member’s death, the EPS also provides a family pension to the surviving spouse and eligible children.

This makes the EPS a vital pillar of your family’s long-term financial security.

If you leave the workforce before completing 10 years of service, you will not receive a monthly pension.

However, your EPS money is not lost.

You can apply for a scheme certificate, which preserves your service history in case you decide to start working again later.

Alternatively, if you do not plan to return to formal employment, you can choose to make a one-time withdrawal of your accumulated EPS funds.

Always consult the EPFO portal to understand your specific pension eligibility status.

Old EPF Scheme vs New EPF Scheme 2026

How do the old and new schemes actually compare side by side?

Many people incorrectly assume that the new laws have reduced their financial benefits.

In reality, the financial math remains largely untouched.

The transformation is entirely administrative and technological.

To illustrate the differences clearly, here is a detailed comparison:

| Feature | EPF Scheme 1952 | EPF Scheme 2026 |

| Legal Framework | Governed by the old 1952 Act | Integrated into the Social Security Code 2020 |

| Contribution Rate | 12% for most establishments | Remains strictly 12% |

| Withdrawal Limits | Confusing, multiple sub-rules | Minimum 25% balance must be maintained |

| Claim Processing | Often took weeks, heavily manual | Digital-first, algorithm-driven faster settlement |

| Job Loss Access | Complex waiting periods | 75% immediately, 100% after 12 months |

| Identity Verification | Manual signatures, physical KYC | Aadhaar-driven biometric linking mandatory |

| Employer Compliance | Traditional physical filings | Stricter digital monitoring and automated penalties |

As the table shows, the core promise of a secure retirement fund remains intact.

The new scheme simply removes the bureaucratic friction that frustrated employees for decades.

Common Mistakes and Actionable Steps

Taking action today will save you from massive compliance headaches tomorrow.

The EPFO system is incredibly efficient when your data is perfect, but it can be highly unforgiving if your records have mismatched information.

Many employees only log into their PF portal when they urgently need money.

By then, it is often too late to fix a naming error or update a dormant bank account.

You must treat your EPF account with the same seriousness as your primary salary bank account.

Updating your Know Your Customer (KYC) details is completely non-negotiable.

First, ensure your UAN is activated and you have the login password. Next, check your basic details.

Does the spelling of your name match your Aadhaar card exactly? Is your date of birth correct?

Are your PAN card and current bank account correctly linked and digitally verified by your employer?

If your bank account changes, you must update it on the EPFO portal immediately.

A mismatched bank account is the number one reason why legitimate withdrawal claims get rejected or delayed.

Have you added a nominee to your EPF account?

This is another critical step that millions of employees simply forget.

If something tragic happens to you, your nominee will face a nightmare trying to claim the funds without an e-nomination.

The new scheme allows you to complete your e-nomination entirely online using your Aadhaar linked mobile number.

You can nominate your spouse, children, or parents, and you can even decide what percentage of the funds each person will receive.

Many employees ignore the tax rules related to their provident fund.

Generally, EPF enjoys the EEE (Exempt, Exempt, Exempt) tax status, meaning the contribution, interest, and final withdrawal are tax-free.

However, there are exceptions. If you withdraw your PF before completing 5 continuous years of service, the amount becomes fully taxable.

Furthermore, if your total employee contribution exceeds ₹2.5 lakh in a single financial year, the interest earned on the excess amount is subject to income tax.

Always consult a tax professional if you make large voluntary contributions to understand your exact tax liability.

How to Check Your PF Balance

Checking your PF balance has become incredibly convenient under the new digital framework.

You no longer need to wait for a yearly statement from your HR department.

Here are the easiest ways to track your money:

- EPFO Member Portal: Log in using your UAN and password to download your detailed monthly passbook.

- UMANG App: The government’s official unified app allows you to view your passbook and raise claims directly from your smartphone.

- SMS Service: If your UAN is registered with your mobile number, send an SMS in the prescribed format to get an instant balance update.

- Missed Call Service: You can simply give a missed call to the official EPFO number from your registered mobile to receive your balance details via text message.

Download your passbook every few months to verify that your employer is depositing the correct amount on time.

If you spot missing months, raise the issue with your company immediately.

Final Thoughts on Your Financial Future

The Employees’ Provident Funds Scheme, 2026, is not a radical overhaul of your finances.

Instead, it is a much-needed modernization of an outdated administrative system.

The government has focused on bringing transparency, speed, and digital efficiency to a process that used to be heavily bureaucratic.

For the average salaried worker, the daily mechanics of the PF deduction will feel exactly the same.

The real benefits become obvious when you try to transfer your account, check your balance, or apply for an emergency advance.

As an employee, your primary responsibility is to stay informed and proactive.

You must take complete ownership of your digital PF identity.

Activate your UAN, link your Aadhaar, update your bank details, and file your e-nomination today.

Do not wait for a financial crisis to realize that your KYC is incomplete.

Your EPF is likely one of the largest financial assets you will build in your lifetime.

By understanding the rules of the New EPF Scheme 2026, you ensure that your retirement corpus continues to grow smoothly, safely, and securely. 🚀

Frequently Asked Questions

What is the new EPF scheme for 2026?

The new scheme replaces the 1952 framework, bringing EPF under the Code on Social Security. It retains the 12% contribution rate but introduces stricter digital compliance, simplified withdrawal rules with a 25% minimum balance mandate, and faster online claim processing.

Is the EPF Scheme 2026 mandatory for all companies?

Yes. If your company has 20 or more employees, it is legally bound to follow the updated EPF regulations under the new Social Security Code.

Has the EPF contribution percentage changed?

No. The standard contribution remains at 12% of your basic salary plus DA. Any contribution above the statutory limit is purely voluntary.

Can I withdraw my full PF amount in 2026?

No, unless you meet specific conditions. You can withdraw 75% if you lose your job, but you must remain continuously unemployed for 12 months to withdraw the final 25% and close the account.

Is the PF wage ceiling increasing in 2026?

Currently, the ceiling remains legally fixed at ₹15,000. While there are strong discussions and proposals to increase it to ₹25,000, no official notification has implemented this hike yet.

Do I need a new UAN under the new scheme?

No. Your existing Universal Account Number remains perfectly valid and will continue to track all your records.

Can I still get money for medical emergencies?

Absolutely. You can request a partial withdrawal for medical treatments, provided you leave a 25% minimum balance in your account.

Is my EPF money completely safe?

Yes. The EPF remains one of the safest, government-backed retirement savings instruments in India. The new scheme only improves its administration and transparency 💡.

Leave a Reply